Following a new ATO ruling, the loss-of-earnings part of a WA workers’ compensation lump-sum settlement is usually taxable, while medical and impairment payments usually are not.

If you are settling a workers’ compensation claim in Western Australia, a recent Australian Taxation Office ruling has changed how some lump-sum payments are treated for tax purposes — and it can materially affect what you actually receive.

WorkCover WA has issued guidance following ATO Class Ruling CR 2025/88, which applies to settlements under the Workers Compensation and Injury Management Act 2023 (WA).

This article explains, in plain English, what the ruling means in practice for injured workers, and where people are most likely to be caught out.

Why this ruling matters for WA workers

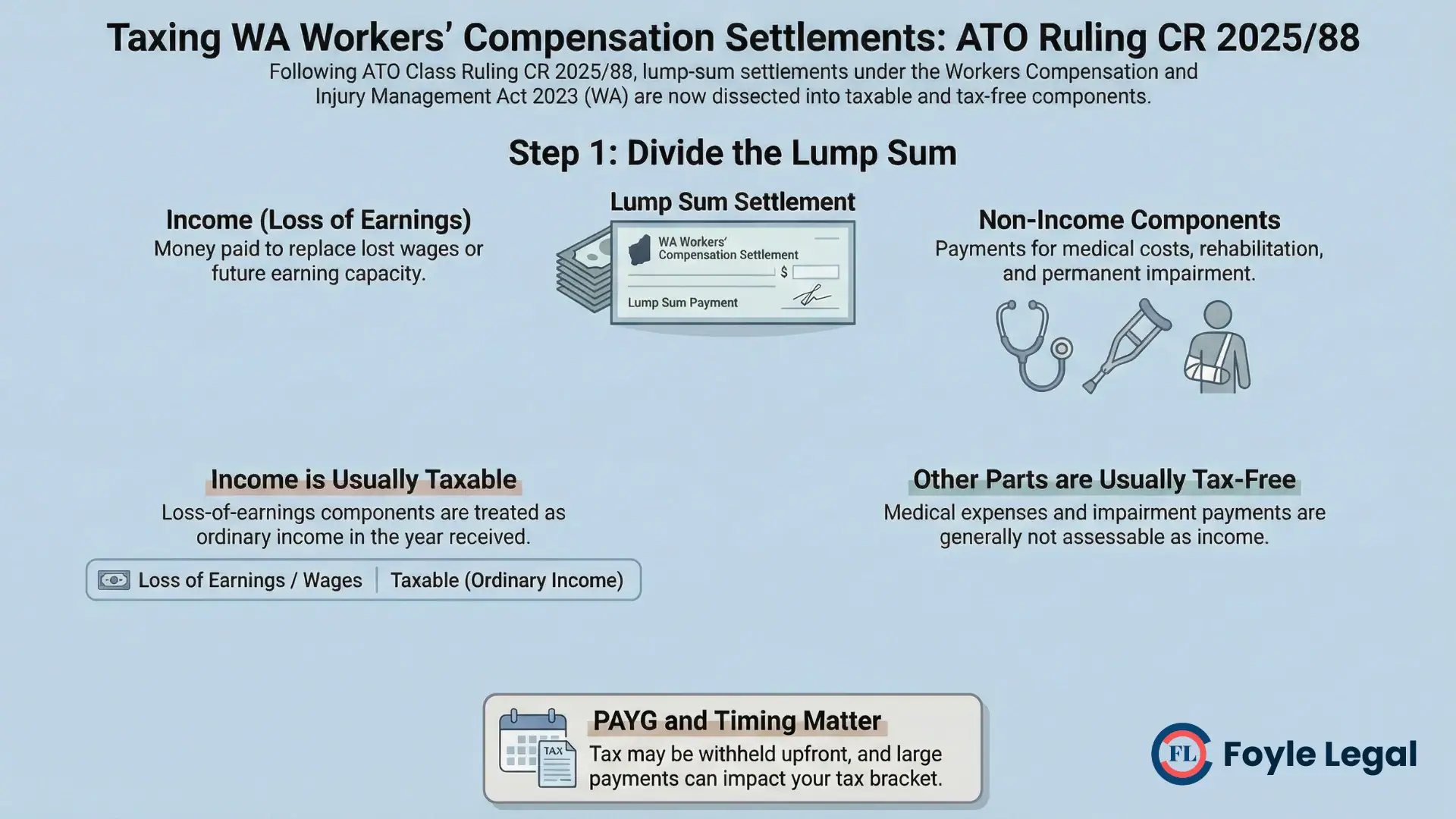

Workers’ compensation settlements in WA often combine multiple entitlements into a single lump sum.

For tax purposes, however, the ATO does not look at the settlement as one amount.

It looks at what each component is replacing.

That distinction is critical, because some components are treated as taxable income and others generally are not.

The key principle: not all settlement components are treated the same

The ATO’s position is based on a long-standing tax principle:

- Payments that replace income are generally taxed as income.

- Payments that compensate for injury, impairment, or expenses generally are not.

Class Ruling CR 2025/88 applies this principle specifically to WA workers’ compensation settlements.

The diagram below shows how the Australian Taxation Office distinguishes between taxable income components and generally non-taxable components in WA workers’ compensation settlements.

How the ATO treats different parts of a WA workers’ compensation lump-sum settlement following Class Ruling CR 2025/88.

Source: Foyle Legal – interpretation of ATO Class Ruling CR 2025/88 (WA workers’ compensation)

How the ATO ruling applies to WA workers’ compensation settlements

1. Loss-of-earnings (income compensation) is usually taxable if paid as a lump sum

If your settlement includes an income compensation component — meaning money paid in place of wages — and that amount is commuted to a lump sum under a registered settlement agreement, the ATO’s view is that it is generally:

- assessable as ordinary income, and

- required to be declared in your tax return in the income year you receive it.

In practical terms, if a lump sum is effectively wages paid in one hit, the ATO will usually tax it the same way wages are taxed. Importantly, the whole amount received for income compensation in a settlement is taxable in that same taxation year.

This applies even though the payment arises from a workers’ compensation claim rather than an employment contract.

For detailed guidance on how loss-of-earnings is calculated in WA personal injury claims, see claiming loss of income after injury.

2. Other settlement components are generally not ordinary income

The ATO’s guidance clearly distinguishes income compensation from other common components of a WA workers’ compensation settlement.

Amounts that are not paid in substitution for wages are generally not assessable as ordinary income and usually do not need to be included in your tax return as income.

These commonly include:

- medical and health expenses

- workplace rehabilitation expenses

- miscellaneous expenses

- permanent impairment compensation

- dust disease impairment compensation

That does not mean tax can never arise in any circumstance — tax law is fact-specific — but in practical terms, the wage-replacement component is the one that most often triggers tax.

For detailed information about how these settlement components are calculated and assessed, see vital aspects of a statutory benefits workers compensation settlement.

3. The real-world impact: why income compensation should be negotiated “gross”

This is where the ruling matters most in practice.

It is very common for injured workers to claim:

- past loss of earnings, and

- future loss of earnings

as part of a settlement.

If the income component of a settlement will be taxed, it should generally be calculated and negotiated on a gross basis, allowing for:

- income tax, and

- the Medicare levy.

If the income component is negotiated as if it were tax-free, the settlement may look acceptable on paper but leave the worker financially worse off once tax is applied.

This is a frequent issue in fast-moving settlements or where tax consequences are not considered early.

Understanding tax implications is just one of many critical considerations. For a comprehensive guide to preparing for settlement, see what you need to know before settling a workers compensation claim.

If you are ever in doubt, please check our WA workers compensation FAQ’s for more detail.

4. PAYG withholding may apply to part of the lump sum

Another practical consequence of the ATO ruling is PAYG withholding.

The ruling indicates that the portion of a lump sum that relates to income compensation may be subject to PAYG withholding by the payer.

Depending on the circumstances, the payer (most commonly the employer, insurer, or self-insurer) may:

- withhold tax from the income compensation component, and

- remit that amount to the ATO on the worker’s behalf.

As a result, a worker may receive less than the headline settlement figure in their bank account because tax has been withheld upfront.

5. Tax rates and Medicare levy: timing matters

Tax is assessed in the income year in which the settlement is received.

A lump-sum payment can push a worker into a higher tax bracket, which means timing can affect the overall tax outcome.

For the 2025–26 income year, Australian resident income tax rates are:

- $0 – $18,200: Nil

- $18,201 – $45,000: 16 cents per dollar over $18,200

- $45,001 – $135,000: $4,288 plus 30 cents per dollar over $45,000

- $135,001 – $190,000: $31,288 plus 37 cents per dollar over $135,000

- $190,001 and over: $51,638 plus 45 cents per dollar over $190,000

These rates do not include the Medicare levy, which is generally 2% of taxable income, subject to exemptions, reductions, surcharges, and individual circumstances.

6. Legal advice and tax advice are not the same thing

At Foyle Legal, our role is to provide legal advice about workers’ compensation claims and settlements under WA law.

Any examples used here are general information only and are not personal tax advice.

If your settlement includes an income compensation component, you should consider obtaining independent advice from a:

- registered tax agent

- accountant, or

- qualified financial adviser

This is particularly important where issues such as PAYG withholding, Medicare levy variations, offsets, deductions, HELP debts, or other income may apply.

As a practical step, tax advice should be obtained before or immediately after settlement, not months later.

7. Simplified examples: how this can play out in WA claims

These examples are simplified and assume the worker:

- is an Australian resident for tax purposes

- has no other income

- has no deductions or offsets

- pays the Medicare levy at 2%

Actual outcomes depend on individual circumstances.

Example 1: Weekly payments followed by a settlement lump sum

Garth is injured at work and receives income compensation equivalent to $80,000 per year.

He settles his claim on 1 January 2026.

In the 2025–26 income year, he has received:

- $40,000 gross in weekly income compensation, and

- $8,209 already withheld and paid to the ATO as PAYG tax.

His settlement includes an additional $70,000 income compensation lump sum.

Total taxable income attributable to income compensation for that year is:

$110,000 ($40,000 + $70,000)

Based on resident tax rates plus the Medicare levy, total tax is approximately $25,988.

After allowing for tax already withheld, Garth would still have around $17,779 more tax to pay, subject to his actual circumstances.

Example 2: No weekly payments, but an income component in settlement

Peacelily lodges a workers’ compensation stress claim that is not accepted and receives no weekly payments (income compensation).

She later resolves the dispute by entering a registered settlement agreement that includes $70,000 for income compensation.

Even though she received no weekly payments, the income compensation component is still treated as ordinary income and included in her tax return in the year it is received.

If she has no other income, the tax payable (including Medicare levy) would be approximately $13,188, less any PAYG withheld.

Bottom line for WA workers’ compensation settlements

If your WA workers’ compensation settlement includes a loss-of-earnings or income compensation component that is paid as a lump sum:

- tax may apply,

- PAYG withholding may reduce what you receive upfront, and

- that component should usually be negotiated on a gross basis.

Understanding this before settlement can materially affect your financial outcome.

Before you finalise your settlement

Identifying tax consequences early can materially affect the net outcome of a WA workers’ compensation settlement, particularly where a lump sum includes income or loss-of-earnings components.

Understanding how income compensation, permanent impairment, and other entitlements are treated under ATO Class Ruling CR 2025/88 can help avoid unexpected tax outcomes and ensure settlement figures are assessed on a like-for-like basis.

Need advice on your WA workers’ compensation settlement?

Foyle Legal assists injured workers across Western Australia with workers’ compensation claims and settlements, including the identification and structuring of income and impairment components. We offer obligation-free consultations and act on a no win no fee basis for eligible WA workers’ compensation matters.

![]()

Get Results for Your Injury Claim!

We Have Hundreds of Client Testimonials Just Like This One!

Get the Compensation You Deserve

Enquire Now, No Obligation

Claim your free initial legal advice worth $580!

Talk to a Real WA Lawyer Today

- No win no fee lawyers – nothing to pay upfront, no hidden costs, and disbursement assistance.

- Top-rated, WA law firm – recognised by clients and peers for our experience, with 300+ 5-star reviews on Google, Facebook and Trustpilot.

- Obligation-free assessment – maximise your fair compensation and we handle your claim end-to-end.

- We help clients to fight back against insurers every day – 100+ years of combined personal injury experience.

Offices in Perth CBD & Malaga. Serve all WA.

Talk to a Real WA Lawyer Today

- No win no fee lawyers – nothing to pay upfront, no hidden costs, and disbursement assistance.

- Top-rated, WA law firm – recognised by clients and peers for our experience, with 300+ 5-star reviews on Google, Facebook and Trustpilot.

- Obligation-free assessment – maximise your fair compensation and we handle your claim end-to-end.

- We help clients to fight back against insurers every day – 100+ years of combined personal injury experience.

Offices in Perth CBD & Malaga. Serve all WA.